Heron Data helped me make better lending decisions in a downturn

- 17th August 2022

Until recently Joe Foster was a Senior Credit Risk Manager at Forward Advances (LON: FWD), one of the UK’s leading Revenue Based Lenders. Prior to this he worked at Barclays in SMB Credit Portfolio Management. At Forward, Joe and his team leveraged Heron Data daily when making credit decisions. We sat down with Joe and wanted to share some of his insights on how Heron Data helped him and his team make smart credit decisions in what is the toughest macroeconomic climate most credit professionals have experienced:

“Underwriting SMBs has historically been expensive and time consuming,” said Joe, “Lenders typically collected bank statements and a set of accounts before calculating ratios and reconciling the bank statements (which are hard to manipulate) with the accounting data (which is not).”

“The result”, as highlighted in the FinRegLab Small Business Spotlight, “is that writing a $100,000 loan costs a traditional financial institution almost the same as writing one for $1,000,000. Since larger loans are typically made to more mature companies they also have lower default rates. These factors worked in tandem to starve newer companies looking for smaller loan sizes of credit.”

“Forward Advances is one of a new wave of lenders who automate their data collection of real time data & reconciliation in order to provide a slick customer experience and reduce operational costs of credit assessment”

NOW MORE THAN EVER YOU WANT GROUND TRUTH

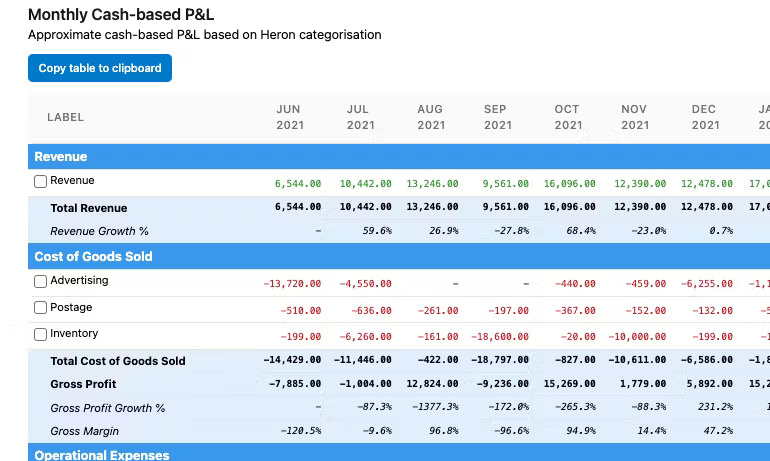

“We know that finding reliable financial information on SMEs has historically been challenging. One reason we loved using Heron-enriched Open Banking data is that it made it 100x faster to take all the revenue that passed through the company’s bank account and compare it to the revenue they reported in their P&L. Private Equity funds pay accountancy firms thousands of dollars and wait weeks for ‘cash proofs’ like this but with Heron we could verify these two disparate data sources against one another in minutes, not days.”

“It didn’t end with revenue – since we primarily lent to small businesses, most don’t have audited accounts. We may or may not agree with how their accountant books revenue, COGS, and other expense items. Heron gave us an unbiased and standardised view into their Gross Profit, Debt Service Coverage, Net Operating Income, and a variety of other metrics. We compared Heron’s output to the numbers which applicants submitted to understand how far they could be out in a worst-case scenario and prioritise applicants for manual review if necessary.”

“Given the current macroeconomic climate, now more than ever you want high confidence in objective information. Even a small inaccuracy in customer-provided information (for example slightly fatter margins or higher revenue than the true number) can affect the outcome of an advance.”

IN TIMES OF UNCERTAINTY, COLLECTIONS START TO MATTER

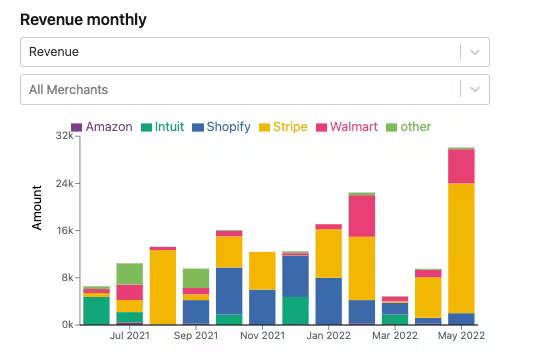

“‘Revenue Based’ lending gets its name because instead of interest and an agreed amortisation schedule, most companies collect their repayment based on customers’ fluctuating revenue. Most lenders are only able to collect revenue from Platforms with which they can integrate directly (e.g. Stripe, Shopify, WooCommerce). These platforms standardise revenue data, making it easy to know how much revenue a company has generated on a given day.”

“A large part of credit risk is really repayment risk: will the customer take longer than expected to repay? If so, the lender bears the cost because of the fixed fee model. If the customer does go under, how much of the advance is outstanding? The less the better.”

“If you can recognise all revenue that flows into a customers’ bank account, you have a larger pool from which you can collect repayments and you can also make a more competitive offer at the point of application. If a customer generates revenue from B2B sales (imagine you are looking a D2C ecommerce brand that get revenue from Shopify but also retails its products in Tesco), being able to collect on the Tesco revenue in addition to that flowing through the online store can decrease your minimum exposure by a significant amount (many months in some cases). In times of uncertainty, collections start to matter more as the market places a higher value on profitability rather than just growth.”

“In a competitive market, recognising a larger revenue pool also enables you to offer lower interest and higher advance amounts. Heron’s platform made it really easy for us to understand ‘true’ revenue beyond what we could pull from our commerce integrations. They gave us balance analytics that also made it 10x easier for us to make sure we collected repayments at the best time to minimise negative events like bounced direct debits”.

UNDERSTANDING CUSTOMERS’ BORROWING STACK IS CRITICAL

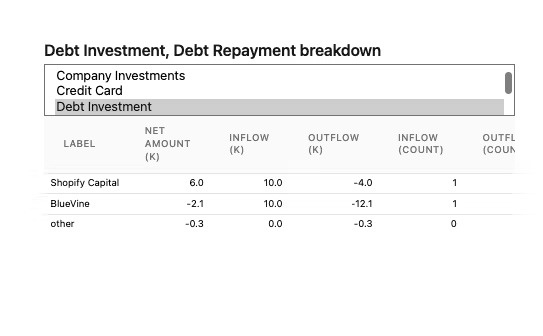

“Revenue based financing is a competitive market, there are multiple players and lots of customers have relationships with other lenders. Understanding who else was in our lending stack, and being able to easily estimate the amount outstanding to each player, made it far easier for us to assess the true risk presented by an applicant. There were multiple cases where the only evidence of a customers’ indebtedness was their bank data because the loans weren’t disclosed by the applicant upfront or present in the other financial statements we collected.”

“In the current climate, insolvency events are more likely than ever. Since pretty much all revenue based lending is unsecured, understanding customers’ borrowing stack is critical. I want to know how many other players were collecting against the same revenue and who else had how much to lose. Heron make this really easy.

About Heron Data

Heron Data supports Fintechs and B2B lenders like Forward Advances, ClearCo, Outfund, Settle, Pipe, and 85+ others to automate loan decisioning with bank transaction data. If you’d like to learn more or are interested in testing us out email [email protected] or book a demo.